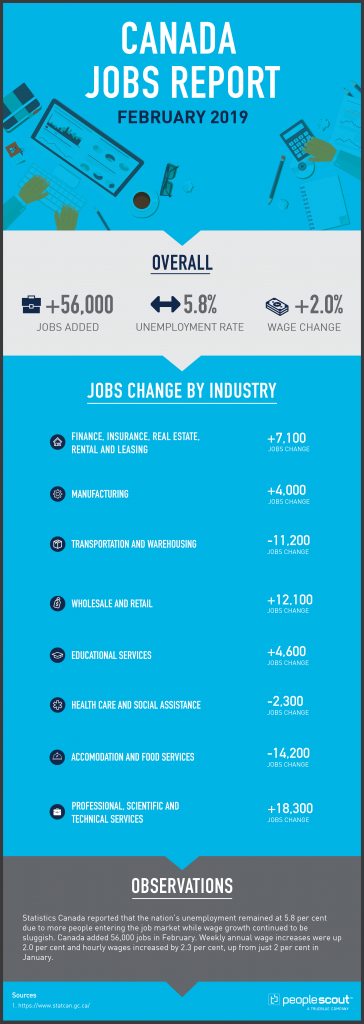

The May 2019 Labour Market Report released by the Office for National Statistics which covers the first quarter of 2019. The unemployment rate dropped to 3.8%, its lowest level since 1974. In that period, 99,000 jobs were added to the UK economy, which was lower than some analysts had projected. Nominal wages rose by 3.3% over the year.

The Numbers

The UK employment rate was estimated at 76.1%, which is higher than the previous year (75.6%) and tied for the highest figure on record.

Estimates for the first quarter of 2019 show 32.70 million employed people who are 16-years-old and over, which is 354,000 more than for a year earlier. This increase is due entirely to an increase in full-time workers. Part-time workers decreased by 18,000 on the year to reach 8.59 million.

The UK unemployment rate was estimated at 3.8%; it has not been lower since October to December 1974.

The UK economic inactivity rate was estimated at 20.8%, lower than a year earlier (21.1%) and close to a record low. Economic inactivity measures people without a job but who are not classed as unemployed because they have not been actively seeking work within the last four weeks and/or they are unable to start work within the next two weeks.

For February to April 2019, there were an estimated 846,000 vacancies in the UK, 28,000 more than a year earlier. Job vacancies are reported on a different schedule than most of the other labour market figures.

Solid Job Numbers, but Lower Than Expected

The addition of nearly 100,000 jobs to the economy is good news by any standard. Yet many economists were expecting even greater increases, and there was speculation about the slowing rate of growth for both jobs and wages. Uncertainty over Brexit is still lurking in the background, as Reuters reports:

“The jobs boom may well reflect how employers have opted to take on workers – who can be laid off quickly during a downturn – rather than commit to longer-term investments while they wait for uncertainty over the conditions of Britain’s departure from the European Union to lift.”

Trouble Ahead?

The idea that employers are choosing to hire expendable workers rather than make long-term capital investments does not suggest confidence in the nation’s economic outlook. Some economists quoted in the Financial Times found some of the data from the May report to be a cause for concern:

“’Britain’s job market continues to defy wider economic uncertainty,’ said Stephen Clarke, senior economic analyst at the Resolution Foundation…

The number of jobs added in the first three months to March was below expectations and lower than the number added in the three months to February. While the number of self-employed increased, the number of full-time employees dropped by 55,000 compared with the previous quarter.

‘Some tentative early warning signs suggest that the jobs market is entering a turbulent period,’ warned James Smith, an economist at ING.

Surprising Growth in the Number of EU Workers

The first quarter of 2019 may well be remembered as a time when Brexit was the dominant topic in every part of the country. Workers for EU countries residing in the UK faced an uncertain future as the original Brexit date loomed. Last year, the ONS reported significant numbers of EU workers leaving the UK in a trend that was nicknamed “Brexodus.”

Yet during this same time, the number of EU nationals working in the UK reached a record high. Nearly 2.4 million citizens of other EU countries now work in the UK, an increase of more than 100,000 compared to the final three months of 2018.

For employers, unexpected shifts such as the reversal of Brexodus underscore the need for expertise in attracting and retaining talent in the uncertain months ahead.