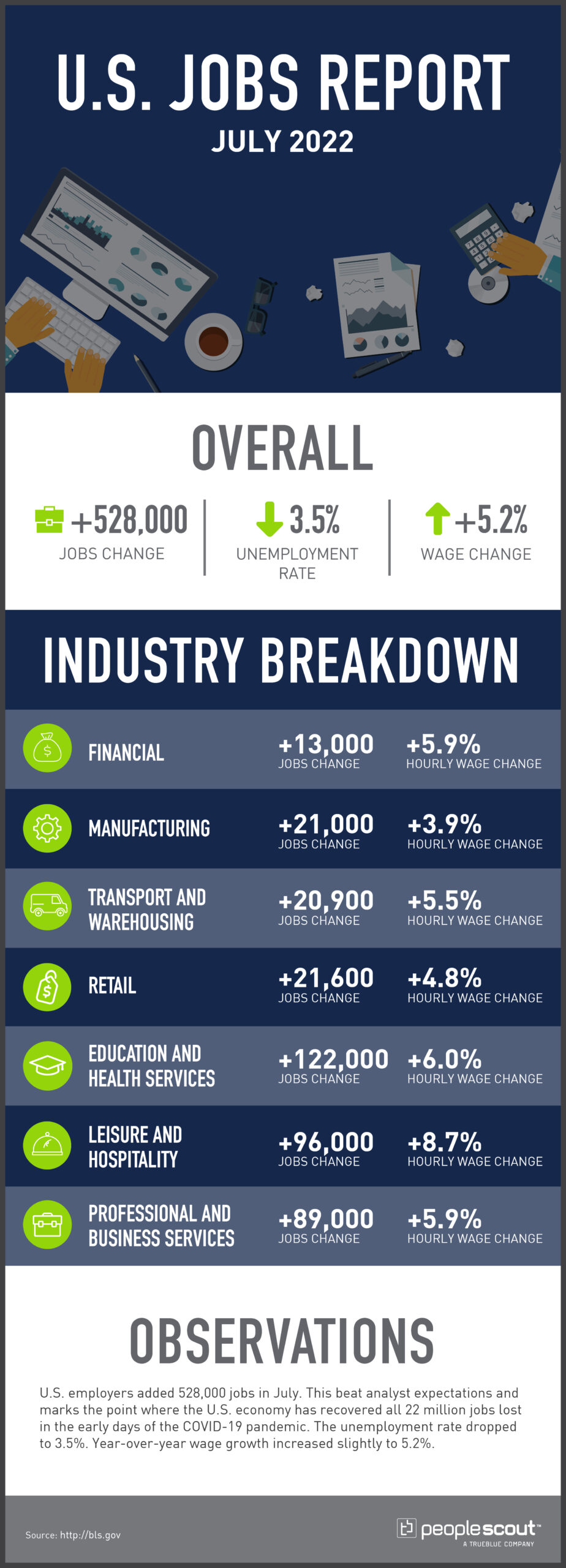

U.S. employers added 528,000 jobs in July. This beat analyst expectations and marks the point where the U.S. economy has recovered all 22 million jobs lost in the early days of the COVID-19 pandemic. The unemployment rate dropped to 3.5%. Year-over-year wage growth increased slightly to 5.2%.

The Numbers

528,000: Employers added 528,000 jobs to the U.S. economy in July.

3.5%: The unemployment rate fell to 3.5%.

5.2%: Wages rose 5.2% over the past year

The Good

The headline from July’s jobs report is the news that after 2.5 years, the U.S. economy has recovered all of the jobs lost early in the pandemic. As the Wall Street Journal reports, this marks the fastest job growth at any point after WWII. The strongest growth took place in the leisure and hospitality; business and professional services; and education and health services sectors. The unemployment rate also fell back to the historic low of 3.5% that we saw right before the pandemic.

The Bad

Despite the good news in July’s report, there is one concerning number. The labor participation rate fell again to 62.1%. As MarketWatch reports, experts would expect the labor participation rate to rise in a strong jobs market, as abundant job openings draw more people into the workforce, especially as there are currently more job openings than there are people looking for work. However, most of the decrease is concentrated in the youngest and oldest workers, those 16-24 and those over 65. This suggests that young workers heading back to school and the retiring baby boomer generation could be behind the drop.

The Unknown

As the New York Times reports, July’s impressive job growth indicates that the U.S. has not entered a recession, despite the fact that the country’s gross domestic product has contracted for the second consecutive quarter. This shows that the economy is withstanding the impact of the Federal Reserve’s aggressive interest rate increases. Economists expect job growth to slow down later in the year as interest rate hikes start to make an impact.